Introduction

Every small business owner reaches a point where numbers stop being just numbers and start telling a story. That story is about survival, growth, mistakes, and success. If you want to truly understand your business, you must understand your finances, and nothing explains financial performance better than an Income Statement.

In this guide, you will not just learn definitions. You will walk through a real-world, practical, and deeply detailed explanation of an Income Statement and how it shapes decisions in small businesses across the United States. This article is written to help beginners, entrepreneurs, freelancers, and growing business owners who want clarity, not confusion.

[Add your focus keyword here]

By the end of this article, you will understand how to read, create, and use an Income Statement to make smarter financial decisions. You will also see a complete Income Statement Example for Small Business and learn how to apply it directly to your own operations.

Understanding the Basics of an Income Statement

What Is an Income Statement and Why It Matters

An Income Statement is one of the most important financial documents in any business. It shows how much money a company earns and spends over a specific period. It answers a simple but powerful question: Is the business making a profit or a loss?

For small businesses, this document is more than just accounting paperwork. It is a decision-making tool. It helps business owners identify strengths, weaknesses, and opportunities for improvement.

An Income Statement typically includes revenue, expenses, and net profit. Revenue represents income generated from sales or services. Expenses include all costs required to operate the business. The difference between revenue and expenses results in either profit or loss.

A well-prepared Income Statement allows business owners to:

- Track financial performance over time

- Identify unnecessary expenses

- Plan future budgets

- Make investment decisions

Without an Income Statement, running a business becomes guesswork. With it, every decision becomes data-driven.

Another important aspect of an Income Statement that many small business owners overlook is its role in building financial discipline. When you consistently review your Income Statement, you begin to develop a deeper awareness of how every dollar flows through your business. This awareness helps you become more intentional with spending and more strategic with revenue generation.

For example, many entrepreneurs focus only on increasing sales, believing that higher revenue automatically leads to higher profits. However, the Income Statement clearly shows that profit depends not only on revenue but also on how well expenses are managed. A business can generate significant income and still struggle financially if costs are not controlled effectively.

Additionally, the Income Statement plays a crucial role in tax preparation. Accurate records ensure that you report the correct income and claim all eligible deductions. This reduces the risk of penalties and helps you optimize your tax obligations legally and efficiently.

Another benefit is improved communication with stakeholders. Whether you are working with investors, partners, or financial advisors, a clear and well-structured Income Statement provides transparency. It builds trust and demonstrates that you understand your business finances.

Over time, reviewing your Income Statement regularly will sharpen your financial instincts. You will start to recognize patterns, anticipate challenges, and identify opportunities before they become obvious. This level of insight is what separates struggling businesses from consistently profitable ones.

Key Components of an Income Statement

Understanding the structure of an Income Statement is essential for accuracy and clarity. Each component plays a specific role in showing the financial health of a business.

The main components include:

Revenue

Revenue is the total income generated from business activities. It is the starting point of the Income Statement. For example, a small bakery earns revenue by selling cakes and pastries.

Cost of Goods Sold (COGS)

This represents the direct cost of producing goods or services. In a bakery, this includes flour, sugar, and other ingredients.

Gross Profit

Gross profit is calculated by subtracting COGS from revenue. It shows how efficiently a business produces its products.

Operating Expenses

These include rent, utilities, salaries, marketing, and other operational costs.

Net Profit

This is the final number on the Income Statement. It shows the actual profit after all expenses are deducted.

Each of these elements must be accurately recorded to ensure that the Income Statement reflects the true financial position of the business.

How Small Businesses Use an Income Statement

Small businesses rely heavily on the Income Statement to guide their operations. Unlike large corporations, small businesses often operate with limited resources, making financial clarity essential.

Business owners use the Income Statement to:

- Monitor monthly performance

- Compare yearly growth

- Identify cost-saving opportunities

- Evaluate pricing strategies

For example, if expenses are increasing but revenue remains constant, the highlights the problem immediately. This allows the owner to take corrective action.

Another important use is securing loans or investments. Financial institutions often require an Income Statement before approving funding.

Common Mistakes to Avoid in Income Statements

Many small business owners make avoidable mistakes when preparing an Statement. These errors can lead to poor decisions and financial confusion.

Common mistakes include:

- Mixing personal and business expenses

- Incorrectly categorizing costs

- Ignoring small expenses

- Failing to update records regularly

Accuracy is crucial. Even small errors can distort the overall picture. A reliable Statement requires consistent tracking and proper accounting practices.

Creating an Income Statement Example for Small Business

Step-by-Step Process to Build an Income Statement

Creating an Income Statement Example for Small Business begins with collecting accurate financial data. This process requires discipline and attention to detail.

Start by gathering all revenue records. This includes sales receipts, invoices, and payment records. Next, list all expenses, including both direct and indirect costs.

The process involves:

- Recording total revenue

- Calculating cost of goods sold

- Determining gross profit

- Listing operating expenses

- Calculating net profit

Each step builds upon the previous one, forming a complete Statement.

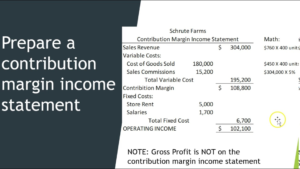

Real Income Statement Example for Small Business

Here is a simplified Statement Example for Small Business:

Monthly Income Statement

Revenue: $15,000

Cost of Goods Sold: $5,000

Gross Profit: $10,000

Operating Expenses:

- Rent: $2,000

- Utilities: $500

- Salaries: $4,000

- Marketing: $1,000

Total Expenses: $7,500

Net Profit: $2,500

This example shows how a business converts revenue into profit. It clearly highlights where money is earned and where it is spent.

Tools and Software for Creating Income Statements

Modern tools make it easier than ever to create an. Small business owners can use accounting software to automate calculations and reduce errors.

Popular tools include:

- QuickBooks

- FreshBooks

- Wave Accounting

These tools provide templates for an Example for Small Business, saving time and effort.

Manual vs Automated Income Statements

Some business owners prefer manual methods, while others rely on software. Each approach has advantages.

Manual methods offer full control and understanding of each entry. However, they require more time and effort.

Automated systems simplify the process and reduce errors. They are ideal for businesses with high transaction volumes.

Choosing the right method depends on the size and complexity of the business.

Analyzing and Interpreting an Income Statement

Understanding Profit Margins

Profit margins are essential for evaluating business performance. They show how much profit is generated from revenue.

The Income Statement helps calculate:

- Gross profit margin

- Operating profit margin

- Net profit margin

These metrics provide insight into efficiency and profitability.

Identifying Financial Trends

A single provides a snapshot, but multiple statements reveal trends. By comparing data over time, business owners can identify patterns.

For example, increasing expenses may indicate inefficiency. Rising revenue may suggest growth opportunities.

Trend analysis transforms the Income Statement into a powerful planning tool.

Using Income Statements for Decision Making

Business decisions should always be based on data. The provides that data.

Owners use it to:

- Adjust pricing

- Reduce costs

- Plan expansions

- Improve operations

Every decision becomes more informed when backed by financial data.

Comparing Income Statements Across Periods

Comparing statements helps measure progress. Monthly and yearly comparisons highlight improvements and setbacks.

This practice ensures that the business stays on track and adapts to changes effectively.

Advanced Strategies for Maximizing Profit Using Income Statements

Reducing Expenses Without Hurting Growth

One of the most effective ways to improve profitability is expense management. The reveals where money is being spent.

Focus on reducing unnecessary costs while maintaining quality.

Increasing Revenue Strategically

Revenue growth is essential for long-term success. The helps identify high-performing products and services.

Invest more in areas that generate the most profit.

Improving Operational Efficiency

Efficiency leads to higher profits. By analyzing the Income Statement, businesses can streamline operations and eliminate waste.

Long-Term Financial Planning with Income Statements

Planning for the future requires accurate data. The provides a foundation for forecasting and budgeting.

It helps businesses prepare for growth and challenges.

Conclusion

Understanding and mastering the Statement is not just an accounting task, it is a fundamental skill that every small business owner must develop to achieve long-term success. Throughout this guide, you have explored not only the structure and components of an, but also how it reflects the real financial story of a business. From tracking revenue and expenses to analyzing profit margins and identifying trends, this single document provides clarity that no guesswork can replace.

For small businesses in particular, financial awareness is the difference between growth and stagnation. A well-prepared Statement Example for Small Business acts as a roadmap, helping you understand where your money is coming from and where it is going. It allows you to make smarter decisions, control costs, and invest confidently in opportunities that drive profit.

Consistency is key. Reviewing your regularly ensures that you stay informed and proactive rather than reactive. It empowers you to catch problems early, adjust strategies, and maintain financial stability even during challenging times.

In the end, success in business is not only about hard work or great ideas, it is about understanding your numbers. When you fully understand your, you gain control over your business future. That control leads to better decisions, stronger growth, and a more sustainable and profitable business journey.

FAQs

What is an Income Statement used for?

An Income Statement is used to track revenue, expenses, and profit over a specific period.

How often should a small business prepare an Income Statement?

Most businesses prepare it monthly and annually.

What is included in an Income Statement?

It includes revenue, cost of goods sold, expenses, and net profit.

Can I create an Income Statement without accounting software?

Yes, it can be created manually using spreadsheets.

Why is an Income Statement important for small businesses?

It helps track financial performance and make informed decisions.

What is the difference between profit and revenue?

Revenue is total income, while profit is the remaining amount after expenses.